Содержание

For example, the cost of antiques or collectibles, fine jewelry, or furs can be determined individually, usually through appraisals. This calculation is not exactly what happened because in this type of situation it’s impossible to determine which items from which batch were sold in which order. Andrew Bloomenthal has 20+ years of editorial experience as a financial journalist and as a financial services marketing writer.

Prepare Stores Account issuing materials according to Last In First Out method assuming the same particulars as in Illustration 1. Issues are to be priced on the principle of ‘First in First Out’. Write out the Stores Ledger Account in respect of the materials for the month of January. It minimizes unrealized inventory gains and tends to show the conservative profit figure by valuation of inventory at value before price rise and provides a hedge against inflation. Product cost will tend to be more realistic since material cost is charged at more recent price.

Imagine if a company purchased 100 items for $10 each, then later purchased 100 more items for $15 each. Under the FIFO method, the cost of goods sold for each of the 60 items is $10/unit because the first goods purchased are the first goods sold. Of the 140 remaining items in inventory, the value of 40 items is $10/unit and the value of 100 items is $15/unit. This is because inventory is assigned the most recent cost under the FIFO method. Typical economic situations involve inflationary markets and rising prices. In this situation, if FIFO assigns the oldest costs to the cost of goods sold, these oldest costs will theoretically be priced lower than the most recent inventory purchased at current inflated prices.

This method of inventory valuation is acceptable under standard accounting practice. This method assumes that the latest receipt of the material in stock is issued first. The assumption that material received last is issued first is only an accounting assumption.

( If average cost method is used:

When a company issues new stock for cash, assets increase with a debit, and equity accounts increase with a credit. To illustrate, assume that La Cantina issues 8,000 shares of common stock to investors on January 1 for cash, with the investors paying cash of $21.50 per share. The company plans to issue most of the shares in exchange for cash, and other shares in exchange for kitchen equipment provided to the corporation by one of the new investors. Two common accounts in the equity section of the balance sheet are used when issuing stock—Common Stock and Additional Paid-in Capital from Common Stock. Common Stock consists of the par value of all shares of common stock issued. This method gives more accurate results than the simple average price method, as it takes into account both the unit prices and the quantities of different materials purchases.

The offemethod assumes that stock received last is issued first that appear in this table are from partnerships from which Investopedia receives compensation. This compensation may impact how and where listings appear. Investopedia does not include all offers available in the marketplace.

Marathon Digital (NASDAQ:MARA) Postpones Results; SEC At Its … – TipRanks

Marathon Digital (NASDAQ:MARA) Postpones Results; SEC At Its ….

Posted: Wed, 01 Mar 2023 09:53:13 GMT [source]

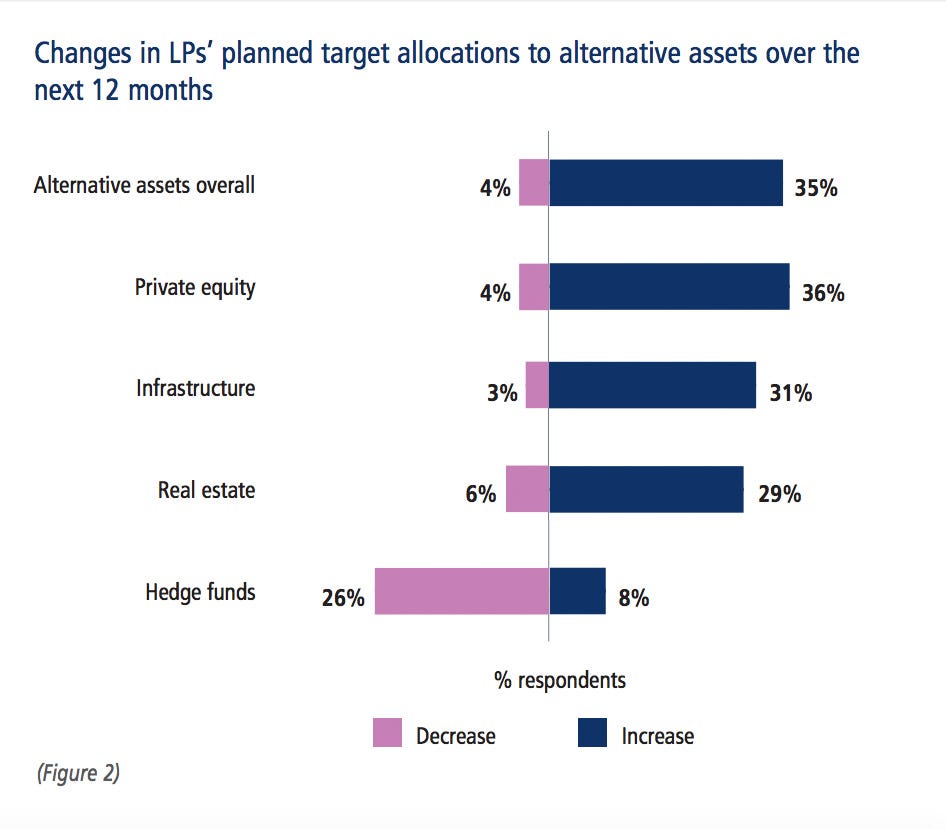

In other words, the beginning inventory was 4,000 units for the period. In contrast, taxes are usually higher under the FIFO method. Assuming that prices are rising, this means that inventory levels are going to be highest as the most recent goods are being kept in inventory. This also means that the earliest goods are reported under the cost of goods sold. Because the expenses are usually lower under the FIFO method, net income is higher, resulting in a potentially higher tax liability. However, please note that if prices are decreasing, the opposite scenarios outlined above play out.

Last in First out | LIFO | Accounting for Materials | Cost Accounting

Under this method material purchased last is issued first. Under this method material purchased first is issued first. Since material is charged at the latest price level the cost of production is realistic. As in the warehouse, all the materials are kept together, there is no sure that the one which was purchased earlier is issued first. The value of the closing stock will increase, resulting in higher profits. Ending inventory is a common financial metric measuring the final value of goods still available for sale at the end of an accounting period.

It should be noted that physical flow of materials may not conform to LIFO assumption. This method is most suitable in times of falling prices because the issue price of materials to jobs will be high while the cost of replacement of materials will be low. But in case of rising prices, this method is not suitable because the issue price of materials to production will be low while the cost of replacement of materials will be high. The average cost method of inventory is also known as weighted average method.

In LIFO, the stock in hand represents, oldest stock while in FIFO, the stock in hand is the latest lot of goods. Although, the assumption is proved illogical and contradictory to the movement of inventory in the business organization. By virtue of this, LIFO method is no longer adopted for valuing inventory.

Last In, First Out Inventory (LIFO) Method Explained

Because shares held in treasury are not outstanding, each treasury stock transaction will impact the number of shares outstanding. A corporation may also purchase its own stock and retire it. Retired stock reduces the number of shares issued. When stock is repurchased for retirement, the stock must be removed from the accounts so that it is not reported on the balance sheet.

Though issues are at current market prices, inventory valuation is not at current market prices. The chief advantage of this method is that, under this method, the materials cost charged to production comes very close to current market price. The cost of production is not accurate but only arbitrary especially when materials prices fluctuate widely. This is because cost of production consists of issue prices of different lots of purchases.

This method ensures the maintenance of a certain minimum amount of stock for emergencies. For pricing a single requisition, more than one price has often to be adopted. For pricing one requisition more than one price has often to be taken. As this method depends on invoices non-receipt of an invoice will obstruct the issue procedure.

FIFO inventory management seeks to sell older products first so that the business is less likely to lose money when the products expire or become obsolete. First In, First Out, commonly known as FIFO, is an asset-management and valuation method in which assets produced or acquired first are sold, used, or disposed of first. Under LIFO, the costs of the most recent products purchased are the first to be expensed. The LIFO method operates under the assumption that the last item of inventory purchased is the first one sold. The greatest disadvantage of this method is that a fresh rate calculation will have to be made as soon as a new lot of materials are purchased which may involve tedious calculations. This method is also useful when transactions are not too many and prices of materials are fairly steady.

Exercise-3 (FIFO, LIFO and average cost method in periodic inventory system)

Therefore, it is important that serious investors understand how to assess the inventory line item when comparing companies across industries or in their own portfolios. When materials are procured for a specific job or a work order, then the actual cost of purchase is allocated to that material supply. The materials procured for a specific purpose are separately market out for the purpose of issue. Using the given transactions prepare a store ledger account by weighted average method. The First-In-First-Out, or FIFO method, is a standard accounting practice that assumes that assets are sold in the same order that they are bought.

Monthly Tax Roundup (Volume 2, Issue 3) – Miller & Chevalier

Monthly Tax Roundup (Volume 2, Issue .

Posted: Wed, 01 Mar 2023 12:00:00 GMT [source]

Such materials will normally be stored separately and issued only to that particular job. In this method, issues are priced at the next price, i.e., price of the material which has been ordered but not yet received. This is an attempt to value issues at an actual price, which is closer to the current market price and should be the replacement price. Materials purchased for a specific job or a batch or process can be identified with the job, batch, or process. Therefore, the job, batch, or process is charged with the actual cost of the material. E.g., a job order for the production of a large compressor is charged with the actual cost of motors and castings purchased specifically for the job.

Also, https://1investing.in/ is not realistic for many companies because they would not leave their older inventory sitting idle in stock while using the most recently acquired inventory. This method assume the principle of conservatism. The materials with highest purchase price are issued is usually followed by materials at the low prices, irrespective of their date of purchase. It presume that, under inflectional situation product can absorb the extra burden of increased prices and thus be allocated leaving low priced materials for deflation.

Starting from the date of their procurement to the date of the issue. So selection of price needs a pricing policy which also facilities in preparation of Costing records. The obvious advantage of FIFO is that it’s the most widely used method of valuing inventory globally. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs. Furthermore, it reduces the impact of inflation, assuming that the cost of purchasing newer inventory will be higher than the purchasing cost of older inventory. Finally, it reduces the obsolescence of inventory.

- One reason for valuing inventory is to determine its value for inventory financing purposes.

- Since the seafood company would never leave older inventory in stock to spoil, FIFO accurately reflects the company’s process of using the oldest inventory first in selling their goods.

- In other words, the total amount paid during a period for various purchases is added up and is divided by the quantity of the material purchased to arrive at a rate for valuing the closing inventory.

- All 2,000 of Batch 1 items are counted at $4.00 each, total $8,000.

- Prepare Stores Account issuing materials according to Last In First Out method assuming the same particulars as in Illustration 1.

This method tends to smooth out the fluctuations in price and reduces the number of calculations to be made, as each issue is charged at the same price until a fresh batch of material is received. This method is not popular because it takes into consideration the prices of different batches but not the quantities purchased in different batches. This method is used when prices do not fluctuate very much and the stock values are small in value.

Example of LIFO vs. FIFO

Textbook content produced by OpenStax is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License . This book uses the Creative Commons Attribution-NonCommercial-ShareAlike License and you must attribute OpenStax. FIFO is the default method of determining inventory value.